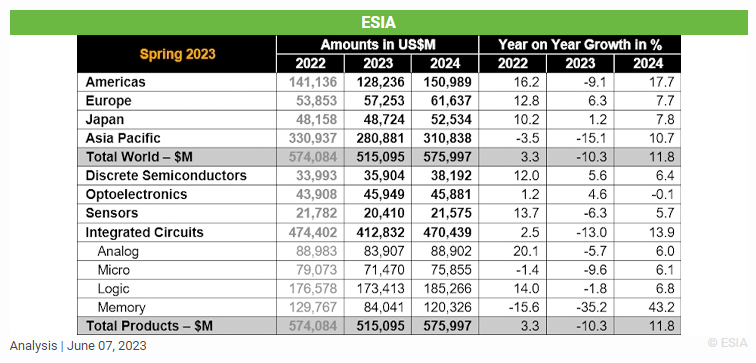

The global semiconductor market is predicted to reach USD 515 billion in 2023, or a downturn of 10.3%. However, this is anticipated to be followed by a robust recovery, with an estimated growth of 11.8% in 2024, reports the European Semiconductor Industry Association (ESIA).

The World Semiconductor Trade Statistics (WSTS) has adjusted its growth projections downwards in response to increasing inflation and weakening demand in end markets, particularly those relying on consumer spending. Although two primary categories, discrete and optoelectronics, are predicted to sustain single-digit year-over-year growth at 5.6% and 4.6% respectively in 2023, other categories are anticipated to shift into negative growth. This includes memory, which is forecasted to decline by approximately 35% year-over-year.

For 2023, the European and Japanese markets are projected to grow, with respective increases of 6.3% and 1.2%. Conversely, the remaining regions are anticipated to face a downturn, with the Americas expected to decline by 9.1% and the Asia Pacific region by 15.1%.

Global market is expected to rebound strongly in 2024

Looking ahead to 2024, the global semiconductor market is forecasted to surge by 11.8%, amounting to USD 576 billion. This expansion will primarily be driven by the memory segment, which is projected to recover to USD 120 billion in 2024, marking an increase of over 40% compared to the previous year. Nearly all other key categories, including discrete, sensors, analog, logic, and micro, are projected to exhibit single-digit growth.

In terms of regional perspectives, all areas are expected to see sustained growth in 2024. Notably, the Americas and Asia Pacific regions are estimated to showcase robust double-digit year-over-year growth.

The electronics components industry, as one of the most dynamic industries on the planet, regularly falls victim to its cyclicality – major swings from oversupply to severe allocations. The past two years have seen the market wrestle with a mix of transportation issues, large increases in demand, and at the same time severe shortages in many component families, some of which still exist today, during the current downturn.